To stave off the mounting effects of global warming, governments and companies around the globe have set an ambitious target of reaching net zero (paring greenhouse gas emissions to nearly zero) by 2050. In the U.S., President Biden wants to achieve 100 percent “clean” electricity by 2035.

These ambitions, however, are set to collide with the realities of the industries and natural resources required to increase electrification. While clean power generation set a milestone in 2021 for wind, utility solar, and battery storage power capacity, the ramp-up in renewable energy may not be coming fast enough, and at the current pace it will only get the U.S. to 35% of the 2035 target.

A clean energy future also will require a vast increase in materials such as lithium, nickel, and copper, that are needed for solar panels, wind turbines, upgrades to electric grids, and electric vehicle (EV) batteries and motors. If all governments follow through on their current pledges, demand for these materials is forecast to double by 2030.

Meanwhile, natural resource companies—an essential supplier of the raw materials for a renewable energy economy—have underinvested for the last decade. While new forces are driving a fresh wave of demand, there is limited supply of the right raw inputs, and the suppliers will need time to regroup and innovate.

This new wave of secular demand is not likely a “super-cycle”—often described as a structural upward shift in demand for every commodity. But we believe there is a case for a sustained investment in those specific natural resources owners and producers that are set to benefit from long-term, positive secular demand trends for the metals that are key inputs into electrification efforts.

APRIL 23 IS THE FIFTY-THIRD CELEBRATION OF EARTH DAY

Global warming, sustainability, and the drive toward renewable energy are some of the major messages being conveyed at events this year for Earth Day. First celebrated in 1970 in the United States, the theme this year is “Invest in Our Planet,” and the events are expected to include one billion participants in more than 190 countries.

Organizers cite renewable energy as one of the most immediate actions to help lower the carbon footprint.

ELECTRIFICATION’S ROLE AMONG RENEWABLES

Electrification is the substitution of electricity generated from renewable energy sources, such as solar, wind, hydropower, and geothermal, for fossil fuel sources such as coal, oil, and natural gas. Its relatively low cost and ease of implementation in many sectors can make it one of the first levers to pull to help meet net-zero goals by reducing emissions such as CO2 (carbon dioxide) and CO2e (carbon dioxide and all the other gases, including methane and nitrous oxide), and by removing CO2 from the air.

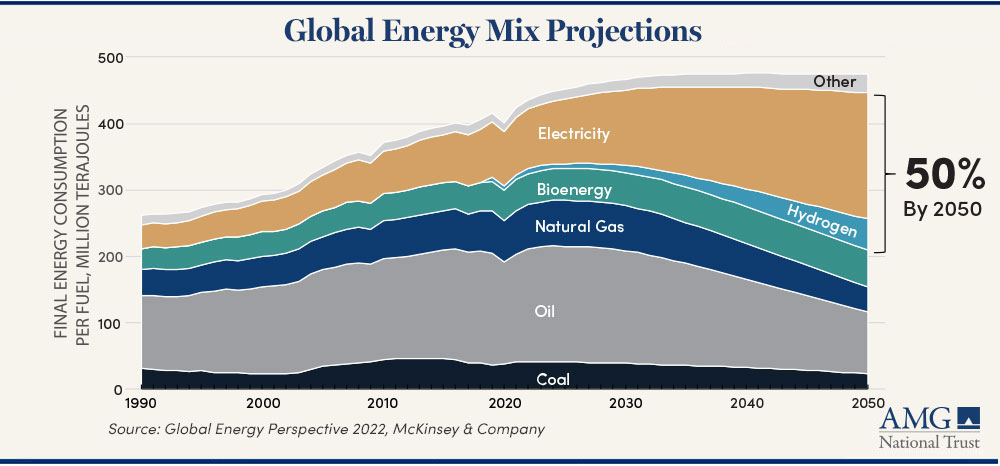

Global agreements have set targets for shifting the world’s energy mix toward renewable sources.

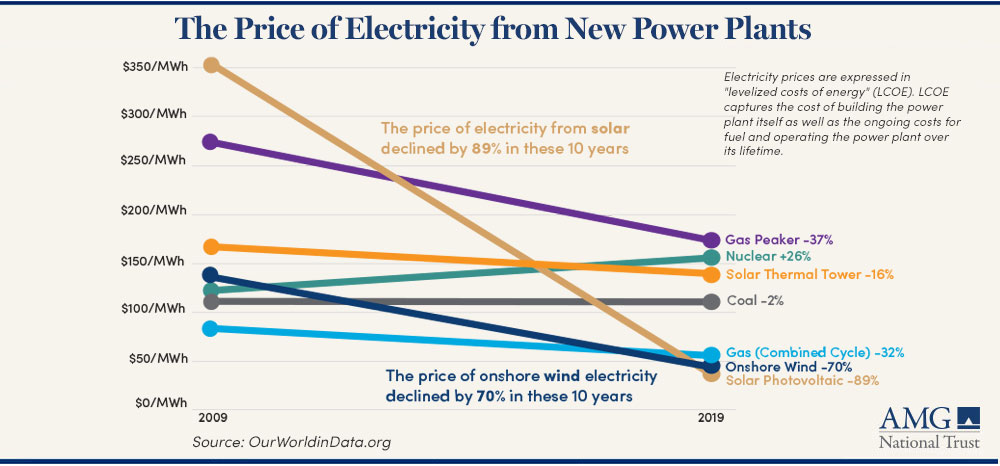

COSTS OF RENEWABLES ARE DECLINING

Upgrading electric grids and battery storage capabilities to match increasing demand remains a work in progress. Costs for solar and battery storage systems are dropping, but they are likely to have to drop significantly for a utility to consider replacing a coal plant with a solar plant. And simply replacing one plant with another that is only slightly cheaper to operate is unlikely to significantly improve productivity. But the technology to make that conversion more affordable and beneficial is on the horizon.

PRIME SECTORS FOR ELECTRIFICATION

Many devices and manufacturing processes (for example, vehicles, appliances, or factory equipment) that require energy to operate can be made to run on electricity, and the opportunities continue to expand with each technological advance. But there are several electrification applications that can be implemented with existing tech.

Electrify home

Driving in and out of your neighborhood each day, you’ve likely come across homes with solar panels attached to the roof. That may be the most visible example of building electrification, and, while the average cost of solar panels in the U.S. is about $16,000, they can also significantly reduce a monthly utility bill.

Energy-saving devices can also make an impact inside a home. For instance, a heat pump can replace other heating and cooling options and be up to three times more efficient, while induction cooktops can increase savings over gas stoves and offer more precise temperature control. Likewise, centralized control of integrated appliances, smart thermostats, and LED bulbs can potentially transform homes into smart homes that are more efficient, safe, and comfortable, based on residents’ habits.

Electric vehicles

Electric vehicles have a smaller carbon footprint than traditional combustion-engine vehicles.

According to the U.S. Bureau of Labor Statistics, the number of EVs on the road has risen from about 22,000 in 2011 to more than two million in 2021, fueled primarily by environmental concerns, performance acknowledgment, greater vehicle choice, cost savings, government policies and better battery storage.

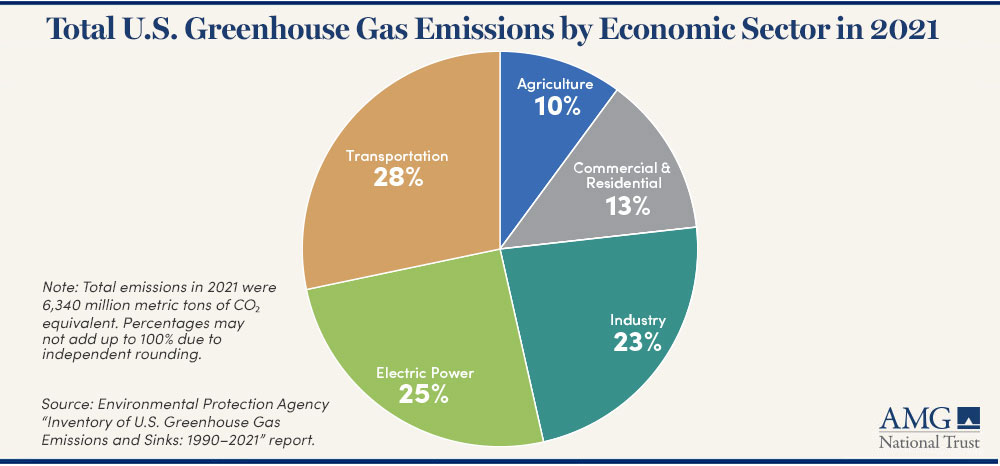

The transportation sector accounts for 28% of U.S. greenhouse gas emissions, so electrifying personal, business, and government vehicle fleets can help achieve global goals.

Electrification of industry

The world’s industrial parks and factories use more energy than any other sector, with about 20 percent coming from electricity. And while electrification of industrial equipment may only be slightly more energy efficient, the cost of maintenance generally is lower. Electrification does not necessarily mean companies must revamp their entire processes. It likely would involve replacing equipment near the end of its service life with newer and more productive electric versions.

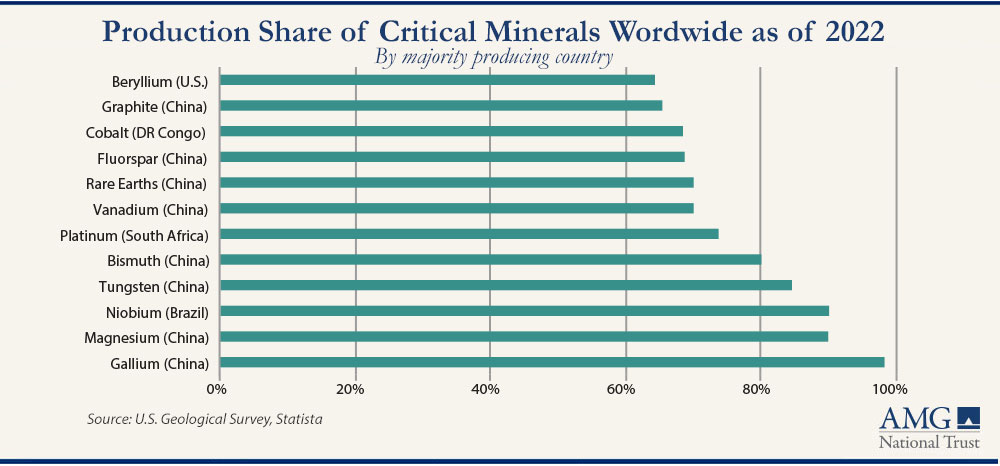

RARE MINERALS AND OTHER RAW MATERIALS IN SHORT SUPPLY

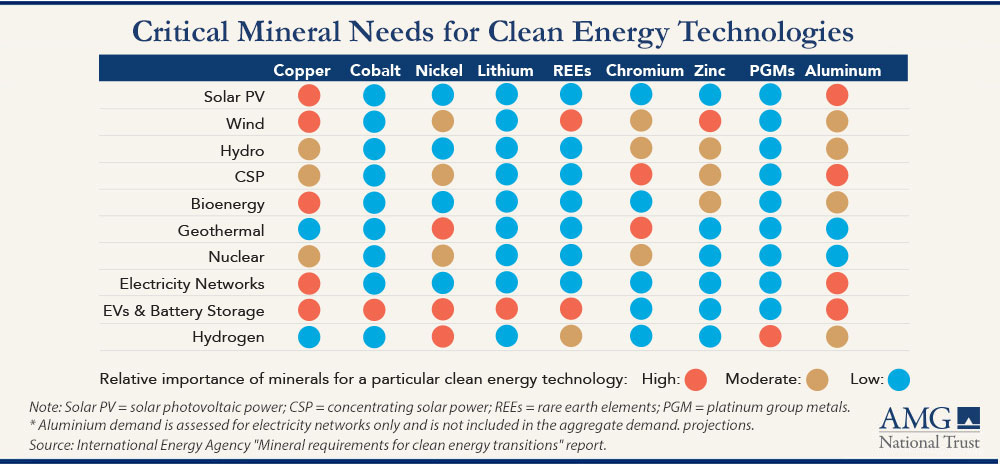

A range of minerals and metals are required to produce solar panels, wind turbines, electric vehicles, and batteries to store electricity. Among them are “rare earth” metallic elements that possess unusual fluorescent, conductive, and magnetic properties, and are so named because of their rarity.

Batteries can require lithium, nickel, cobalt, manganese, and graphite. Electrification uses copper and aluminum primarily. Rare earth elements are needed for magnets in wind turbines and the motors of electric vehicles, among other uses.

Competition for these elements can be fierce, as they also are needed for computer screens, cellphones and countless other electronic devices. Recycling rare earth elements is an option, but the process can be difficult and “dirty” for the environment.

The natural resources industry, meanwhile, has grappled with underinvestment since prices—along with several companies—collapsed a decade ago. COVID-19, inflation and the war in Ukraine have also pressured the industry, as well as environmental, social, and governance (ESG) factors that may tend to rank mining companies poorly and send investors elsewhere.

A further complication is that some of these known rare earth mineral or metal deposits are highly concentrated in a few countries or are controlled by China.

But deposits are likely all over the world, and several mining exploration companies are searching for them in the U.S., which ranks seventh in the world in estimated rare earth reserves, behind China, Vietnam, Brazil, Russia, India, and Australia.

Producing EVs also currently consumes a large amount of raw materials and could require anywhere from six to 30 times the current supply of key minerals to meet industry needs. At least one EV maker, though, is turning to motors that do not require these key minerals.

RENEWABLE ADVOCATES URGE MORE INVESTMENT

Renewable energy growth set a record in 2021, and was on pace to do so again in 2022. To maintain this momentum, it’s estimated that at least $4 trillion a year needs to be invested in renewable energy until 2030. The benefit from the reduction of pollution and climate impact, though, is forecast to be up to $4.2 trillion per year.

Meeting a 2035 timeline will also require a robust supply of the raw materials needed to build out a network of wind turbines, solar power, electric grids and other key components of electrification.

HOW AMG CAN HELP

Talk to your advisor about your situation, cash need and risk tolerance on navigating this tricky environment.

Not a client? Find out more about AMG’s Personal Financial Management (PFM) or to book a free consultation call 303-486-1475 or email us the best day and time to reach you.