There’s a belief that wealthy Americans do a poor job of talking to their children and grandchildren about money. A supposed curse has even arisen around the transfer of generational wealth: 70% of wealthy families are likely to lose their wealth by the second generation. By the third generation, that can jump to 90%. Some express this as “shirtsleeves to shirtsleeves” in three generations.

Our experience is quite different. From nearly 50 years of helping families build, manage, and pass down wealth, we at AMG have found that most clients want to take steps to protect their wealth for the next generations—and seek advice to do so. More importantly, they actively include the next generation in their wealth-management journey, and communicate their decisions, values, and goals.

A first-generation wealth builder has many decisions to make, including how to prepare the second and third generations to eventually handle the family fortune. Unpreparedness can be a recurring theme among studies of the issue: Only about one-fourth of affluent investors feel they have kept heirs very well informed about future wealth; on the flip side, heirs may consider themselves unready to handle their pending wealth.

With a generational wealth transfer looming as Baby Boomers age, wealthy Americans and their families likely will be under increasing pressure to manage the challenges of wealth transfer and multi-generational wealth preservation.

NATIONAL TEACH CHILDREN TO SAVE DAY

#TeachChildrentoSaveDay is observed on the fourth Thursday in April (April 24 this year) as part of Financial Literacy Month and is a great time to teach financial literacy lessons that can span generations.

Children generally start to form their views on money early on, and parents often can have the most influence on them. Children who have regular money talks with their parents at least once a week are more likely to have more positive money behavior and expectations. That positive behavior can be reinforced by allowing children to, in an age-appropriate way, make money decisions early on.

Doing so models positive financial skills and values that can help your children to extend the family’s wealth to another generation when they become parents.

THE GREAT WEALTH TRANSFER

The spigot of inheritances is about to be thrown wide open in the so-called Great Wealth Transfer—perhaps the largest wealth transfer in history. One estimate is for $72.6 trillion in assets to be passed down to heirs by the Baby Boom generation through 2045. Another $11.9 trillion is expected to be gifted to charities.

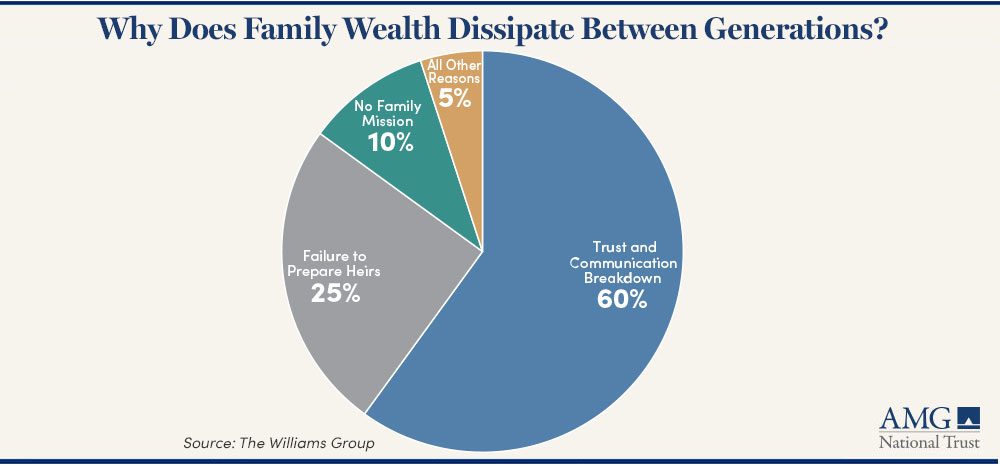

Why wealthy families may lose their fortunes

If you talk to families that have seen their wealth dwindle among subsequent generations, they may blame investments that went bad, poor counseling from legal or financial advisors, or perhaps inadequate tax planning.

Wealth advisors, on the other hand, often say the root cause is not only the failure of one generation to have in-depth discussions with the next about the family’s wealth, values, and legacy goals, but also whether the next generation is willing to listen.

It can also be attributed to changes in family values and focus. The single-mindedness that motivated the initial wealth creators may be directed toward a different interest by the next generation. There is often a benefit to growing up with wealth in that the next generations have the ability to pursue interests or opportunities different from the source of the family’s initial wealth.

HOW TO PROTECT AND PASS DOWN GENERATIONAL WEALTH

Regardless of net worth, all families can take steps to prepare their estates for transitioning from one generation to another. Avoiding the “shirtsleeves to shirtsleeves” pitfall will require dedicated planning and education among generations—not just the immediate heirs but also, if they are old enough to understand, the generation after that.

- Share your values and money smarts

- Build a plan for passing wealth to the next generation

- Communicate your wealth transfer plan

Share your values and money smarts

Early on and woven into your family values, children and grandchildren can be taught the basics about money and what can be done with it, e.g., saving, spending, or gifting. One way to assess how they absorb these lessons is to give them a small amount of money, then talk to them later about what they did with it.

Keep in mind that everyone is different about listening to advice. Some pay attention. Some don’t listen. Some won’t listen. The objective should be to give them a chance to grow into their own person rather than have them feel overwhelmed with the responsibility of being good stewards of the family’s wealth.

Consider that children generally are closer to their parents than to grandparents. How generation two (Gen 2) passes along these money-management lessons—or even whether they present them at all—will likely affect generation three’s (Gen 3’s) approach to handling wealth.

Much like the children’s game “Pass It On,” where a simple message is whispered into the ear of the next child in line and often becomes distorted before it reaches the last one in line, the lessons may vary or break down when passed from Gen 2 to Gen 3. The result may be that Gen 3 does not have a strong enough relationship with grandparents to hew to their values, wishes, or goals.

In addition to staying in the lives of Gen 3 to pass along values, grandparents can also build safeguards into their estate plans through the thoughtful structure of trusts.

RELATED ARTICLE: End of Life Planning: Are You Good to Go?

Build a plan for passing wealth to the next generation

An estate plan may help to minimize wealth-transfer taxes and can be used to control when and how assets are distributed to individuals or organizations such as charities.

When designing an estate plan, using trusts can be beneficial in instances such as when Gen 1 recognizes that the heirs in Gen 2 may not be equally ready to handle a large inheritance. One child may be fully capable; another may be capable but occupied with a job or raising their own family; and one may have an addiction or require extended care. Or perhaps an heir lives beyond their means and makes excessive requests for cash.

A possible solution is for Gen 1 to set aside the same amount for each heir, and differentiate the trust’s terms to dictate how much, when, and how assets are distributed based on the beneficiaries’ actions or habits.

Many other unique or unexpected family circumstances can be dealt with through a trust:

- Gen 1 may be able to protect assets from a divorce by placing them in a trust.

- A grantor might place business interests in a trust, and subsequently have the trust sell those interests. The money could sit in the trust, tax-advantaged, until the next generation is ready to embark on their own careers.

- Gen 1 may want to share part of their wealth with Gen 2 or Gen 3 during their lifetime. Gen 1 can take advantage of the annual gift tax exclusion of $19,000 (2025) or shift significant assets out of their estate using the lifetime gift tax exemption of $13.99 million (2025) by making planned gifts to trusts, which can be designed to distribute assets to heirs.

- If Gen 1 is the head of a blended family with potentially conflicting goals, Gen 1 might wish to treat children and stepchildren differently, particularly if the stepchildren will inherit assets from a biological parent. If there are children of vastly disparate ages, a trust can be used to divide assets into separate family groups with different inheritance schedules.

Communicate your wealth transfer plan

Some of us enjoy surprises. But holding back information about, for instance, your finances, will or succession plans can be a recipe for conflict among heirs.

If you are Gen 1, you should consider involving Gen 2 and, if possible, Gen 3 in discussions early on. Lay out a family mission statement of what you envision in terms of spending, saving, and philanthropy. If you don’t wish to discuss specific dollar amounts, at least share an outline of your will and trust. Doing so can be a valuable reality check for heirs and allows you to explain the rationale behind goals and decisions.

At AMG, we suggest everyone meet with the family’s wealth advisor periodically; some clients have required their heirs to do so. We’ve found that these meetings can spark helpful conversations and allow the advisor to understand everyone’s thinking.

Be mindful that not talking about who gets what because you wish to avoid hurt feelings can have the opposite effect after you are gone—and when adjustments no longer are possible. The heirs will find out most things eventually.

Also, it may be helpful to explain the choices for executor, trustee, guardian, power of attorney or any other key role. The individuals selected for those roles may need time to prepare.

If you wish to instill a legacy of charitable giving, one option is to use a donor-advised fund, like the AMG Charitable Gift Foundation. You could set aside, for example, a sum for each child or grandchild to direct to charity, with the caveat that they explain their rationale. Gifts to a donor-advised fund are typically irrevocable and generally tax-deductible in the calendar year gifted. Grants from the donor-advised fund typically must be made to qualifying charitable organizations.

How you prepare your children to handle wealth will be a guidepost for how they educate subsequent generations. Most importantly, what you would like your wealth to accomplish now and into the futures should be an ongoing conversation.

HOW AMG CAN HELP

We at AMG believe estates and trusts should be part of comprehensive wealth planning that encompasses a client’s total financial picture and provides for all needs at all life stages, from wealth accumulation, investments, and education planning to retirement income and wealth transfer.

For over 50 years, AMG has been a trusted resource for many families, especially those with complicated financial lives. We’re here to help you build and manage your wealth through integrated financial planning, investment management, access to private capital, tax preparation, trust administration, charitable giving, retirement plan administration, and banking services. To find out more about AMG’s Personal Financial Management (PFM) or to book a free consultation call 303-486-1475 or email us the best day and time to reach you.